Table of Contents

It seems that all modern technological innovations go through some kind of hype cycle. The best known is the dotcom bubble from the late 1990s and early 2000s. The Nasdaq more than doubled between early 1997 and its peak in March 2000. Many think an artificial intelligence (AI) bubble is now forming; many others disagree. One of the key differences between companies now and those during the dot-com bubble is profitability.

While many technology companies at the time had little revenue and no profits, there were dozens of them companies in the AI industry today they are cash flow positive, have rising sales, or are highly profitable – and not just hyped. This is a crucial distinction that can help you with your investment strategy. Here are two companies that fit this model.

Micron technology

If there’s one thing AI needs, it’s data, and this data needs memory – lots of it. Micron (NASDAQ:MU) is a global leader in providing DRAM (dynamic random access memory) and NAND (flash memory), used in smartphones, PCs, memory cards, data centers, etc. After a difficult 2023 fiscal year, Micron is back in a big way.

In fiscal 2023, Micron faced geopolitical issues that hampered Chinese sales and a market where there was no demand for its products due to oversupply. In other words, many of its customers used existing inventory instead of buying more from Micron. Revenue fell from $31 billion in fiscal 2022 to $16 billion in fiscal 2023. The industry is cyclical; by 2023 it was down, but now things are looking better.

AI is driving two trends that will be tailwinds for Micron. First, hundreds of data centers are coming online every year, and this trend is expected to continue for many years to come. Micron management says sales of HBM (high-bandwidth memory) will reach hundreds of millions this fiscal year and “several billions” next fiscal year. Next, AI will increase the demand for upgrading PCs and smartphones, and these AI-ready systems will require more memory, a direct benefit to Micron.

Micron reported revenues of $6.8 billion in the third quarter of fiscal 2024, an increase of 81% year-over-year and significant margin improvement due to high demand. Operating income improved year over year from a loss of $1.8 billion to a profit of $719 million.

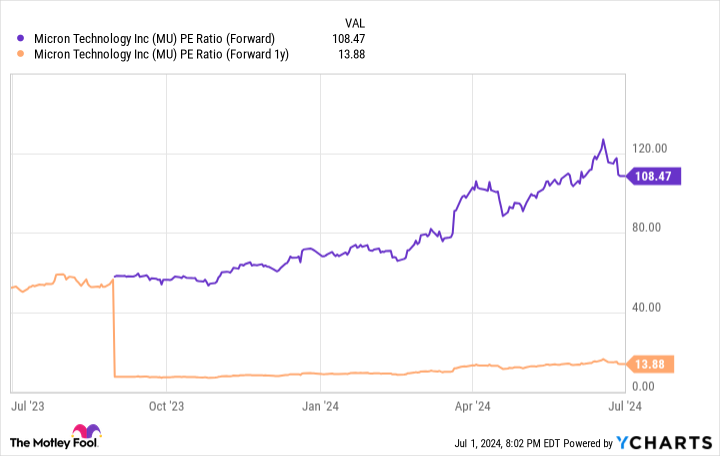

The stock’s valuation has spiraled out of control due to last year’s profitability and gradual recovery this year. Analysts’ average expectations for earnings per share (EPS) this year are just $1.23, giving Micron a price-to-earnings (P/E) ratio of over 100 at the current price; However, this is not the whole story. As shown below, analysts are predicting a huge increase in earnings per share to $9.48 next year, which would bring the price/earnings to just 14.

The low valuation based on fiscal 2025 estimates and significant tailwinds make Micron a solid long-term investment.

CrowdStrike

Cybersecurity is always a priority for executives because the cost of breaches, in terms of direct costs, downtime, remediation, etc., can be enormous. Most successful breaches occur through endpoints, so companies are clamoring for AI-powered protection CrowdStrike‘S (NASDAQ: CRWD) Falcon platform.

Falcon is completely cloud-based and modular, so companies can add features as needed. Selling additional modules is part of CrowdStrike’s land-and-expand sales strategy, which is working well. As of Q1 FY25, 65% of customers were using at least five modules, and 28% were using seven or more.

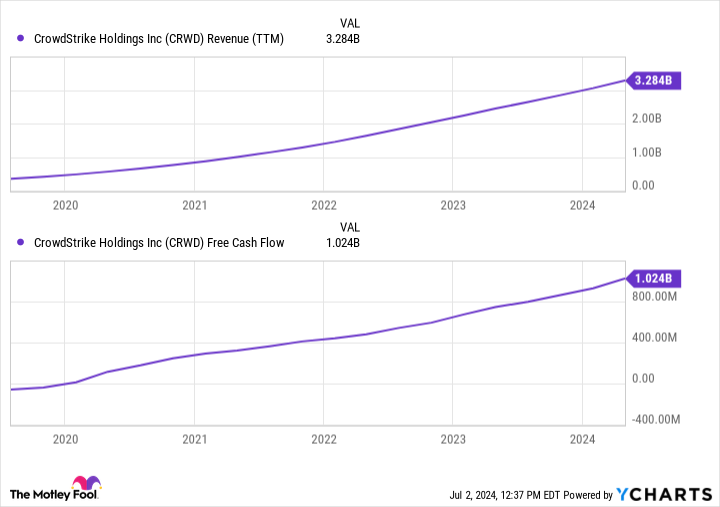

Demand for endpoint protection is driving incredible growth in CrowdStrike’s revenue and free cash flow, as shown below.

The incredible sales growth and free cash flow margin of almost 32% in the last twelve months show why investors are buying the stock overwhelmingly. The stock is up 50% so far in 2024 and 500% in the past five years. However, the epic rise has made the stock’s price-to-sales ratio (P/S) extremely high.

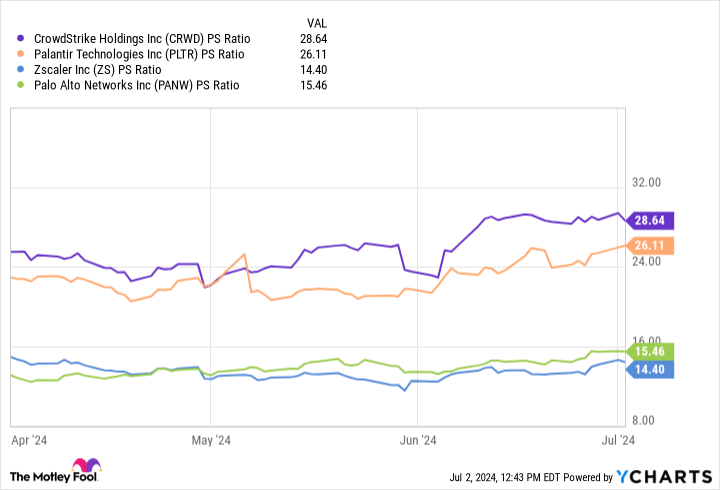

CrowdStrike’s P/S ratio is now almost 29, higher than that of any other fast-growing software company Palantir and cybersecurity companies love it Palo Alto Networks And Zscaler:

CRWD PS ratio data Ygraphs

Investors should be cautious about buying CrowdStrike due to its valuation; However, the company’s results are spectacular and it has a great future.

The artificial intelligence boom is in full swing and many companies are reaping the benefits. Tech investors: keep Micron and CrowdStrike on your radar.

Should You Invest $1,000 in Micron Technology Now?

Consider the following before purchasing shares in Micron Technology:

The Motley Fool stock advisor The analyst team has just identified what they think is the 10 best stocks for investors to buy now… and Micron Technology wasn’t one of them. The ten stocks that survived the cut could deliver monster returns in the coming years.

Think about when Nvidia created this list on April 15, 2005… if you had $1,000 invested at the time of our recommendation, you would have $786,046!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including portfolio building guidance, regular analyst updates, and two new stock picks per month. The Stock Advisor is on duty more than quadrupled the return of the S&P 500 since 2002*.

*Stock Advisor returns July 2, 2024

Bradley Guichard has positions in CrowdStrike, Micron Technology and Palo Alto Networks. The Motley Fool holds positions in and recommends CrowdStrike, Palantir Technologies, Palo Alto Networks, and Zscaler. The Motley Fool has one disclosure policy.

2 Rising Artificial Intelligence (AI) Stocks That Aren’t Just Hype was originally published by The Motley Fool