Table of Contents

Over the past year, investors have turned to the ‘Beautiful seven“Stocks looking for outsized gains, and for good reason.

Mega-cap tech companies such as Nvidia, Microsoft, AlphabetAnd Metaplatforms have all outperformed the S&P500 And Nasdaq Composite during the past 12 months. Many of these gains can be attributed to increasing interest in artificial intelligence (AI), a market dominated by the Magnificent Seven.

But despite the impressive performance of the above companies, I see another member of the Magnificent Seven as a superior choice for long-term investors.

E-commerce and cloud computing giant Amazon (NASDAQ: AMZN) has underperformed the Nasdaq over the past year and has actually generated returns in line with the S&P 500.

With shares down about 14% over the past month, I think this is a prime opportunity to buy the dip in Amazon.

Let’s take a look at how Amazon is quietly disrupting the AI landscape and assess why it now seems like a lucrative opportunity to acquire stock at a dirt-cheap valuation.

Don’t call it a comeback

One of the biggest opportunities surrounding AI is cloud computing. Amazon faces stiff competition in the cloud infrastructure market from Microsoft Azure and Alphabet’s Google Cloud Platform (GCP).

Over the past 18 months, Microsoft has rapidly expanded the Azure platform with its $10 billion investment in OpenAI, the developer of ChatGPT. Additionally, Alphabet has made a respectable break into the cloud space through a series of acquisitions, including MobiledgeX, Forseeti, Siemplify and Mandiant.

These moves by Microsoft and Alphabet initially seemed to take a toll on Amazon’s revenue growth and profitability in the cloud sector. However, the table below illustrates some new encouraging trends in Amazon’s cloud segment, Amazon Web Services (AWS).

|

Category |

Q1 2023 |

Q2 2023 |

Q3 2023 |

Q4 2023 |

Q1 2024 |

Q2 2024 |

|---|---|---|---|---|---|---|

|

AWS revenue year over year % growth |

16% |

12% |

12% |

13% |

17% |

19% |

|

AWS Operating Income year-over-year % growth |

(26%) |

(8%) |

30% |

39% |

83% |

72% |

Data source: Investor Relations

The above figures show a very positive story for Amazon. Over the past year, AWS has gone from a company experiencing consistent slowdowns to one that has now grown for three consecutive quarters while significantly increasing operating income.

Amazon is a money printing machine

It’s nice to see a return to sales and profit growth, but it’s only part of the bigger story for Amazon.

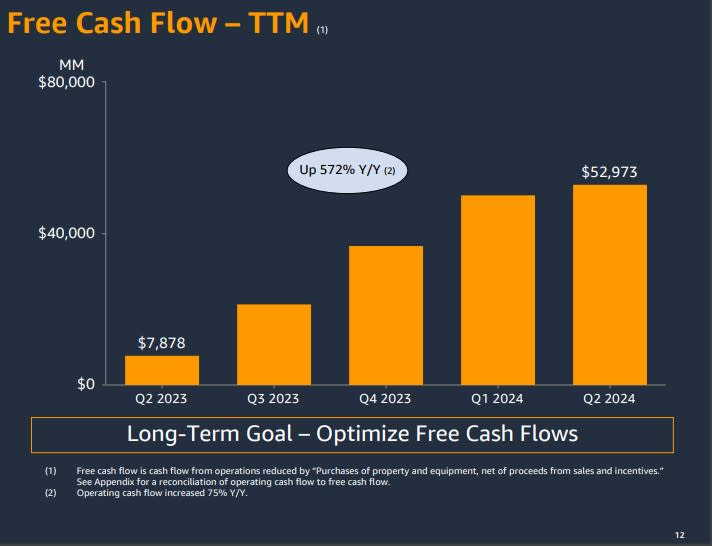

The majority of Amazon’s operating profits come from AWS. For this reason, the reacceleration of its cloud business has had a direct impact on Amazon’s overall cash flow profile. For the quarter ended June 30, Amazon generated $53 billion in free cash flow over the trailing twelve months. Moreover, with a balance sheet of $86 billion in cash and equivalents, Amazon has virtually no shortage to invest aggressively and give its rivals a run for their money.

One of the catalysts for AWS’s renewed growth is Amazon’s $4 billion investment in generative AI startup Anthropic.

This relationship is especially important because Anthropic trains its AI models on Amazon’s internal semiconductor chips – Trainium and Inferentia. This gives Amazon a direct line to compete with Nvidia as demand for semiconductor chips continues to grow.

Additionally, the company is also investing $11 billion in a data center project in Indiana. To me, these investments strengthen Amazon’s ambitions to compete across the AI landscape as AWS enters a new phase of its evolution.

For these reasons, I think AWS’s revenue growth and renewed profits shown above are just the beginning.

An excellent appreciation for investors

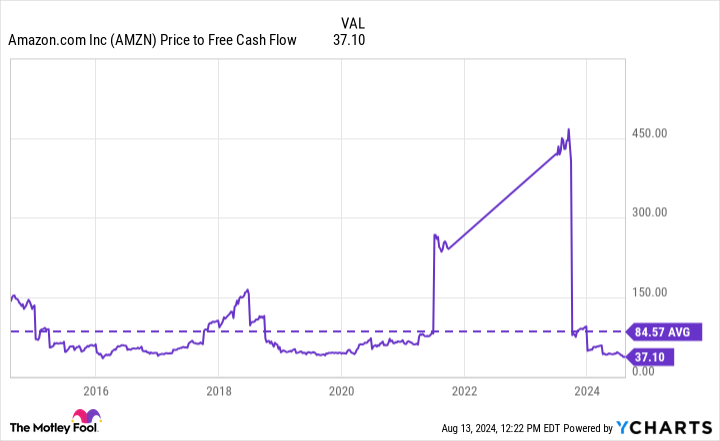

Amazon currently trades at a price-to-free-cash-flow (P/FCF) multiple of 37.1, which is less than half its 10-year average. I find this odd, considering that Amazon is a much larger and much more sophisticated company today than it was a decade ago.

To me, investors are overlooking or not appreciating Amazon’s dive into the AI world. I think the future potential of AI could be baked into some of Amazon’s Magnificent Seven compatriots, as many of them have outperformed the markets by a wide margin over the past year.

Amazon, on the other hand, is already reaping the benefits of these AI-driven initiatives, and the company has a wealth of cash to continue funding its growth for quite some time to come. For these reasons, I think Amazon is the most lucrative opportunity among mega-cap tech stocks right now. In my view, this is an excellent opportunity to buy Amazon stock by hand.

Should You Invest $1,000 in Amazon Now?

Before you buy stock in Amazon, consider this:

The Motley Fool stock advisor The analyst team has just identified what they think is the 10 best stocks for investors to buy now… and Amazon wasn’t one of them. The ten stocks that survived the cut could deliver monster returns in the coming years.

Think about when Nvidia created this list on April 15, 2005… if you had $1,000 invested at the time of our recommendation, you would have $763,374!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including portfolio building guidance, regular analyst updates, and two new stock picks per month. The Stock Advisor is on duty more than quadrupled the return of the S&P 500 since 2002*.

*Stock Advisor returns August 12, 2024

Suzanne Frey, a director at Alphabet, is a member of The Motley Fool’s board of directors. Randi Zuckerberg, former director of market development and spokeswoman for Facebook and sister of Mark Zuckerberg, CEO of Meta Platforms, is a member of The Motley Fool’s board of directors. John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Adam Spatacco has positions in Alphabet, Amazon, Meta Platforms, Microsoft and Nvidia. The Motley Fool holds positions in and recommends Alphabet, Amazon, Meta Platforms, Microsoft and Nvidia. The Motley Fool recommends the following options: long January 2026 $395 calls to Microsoft and short January 2026 $405 calls to Microsoft. The Motley Fool has one disclosure policy.

If I could only invest in one ‘Magnificent Seven’ stock over the next ten years, this would be it was originally published by The Motley Fool