Table of Contents

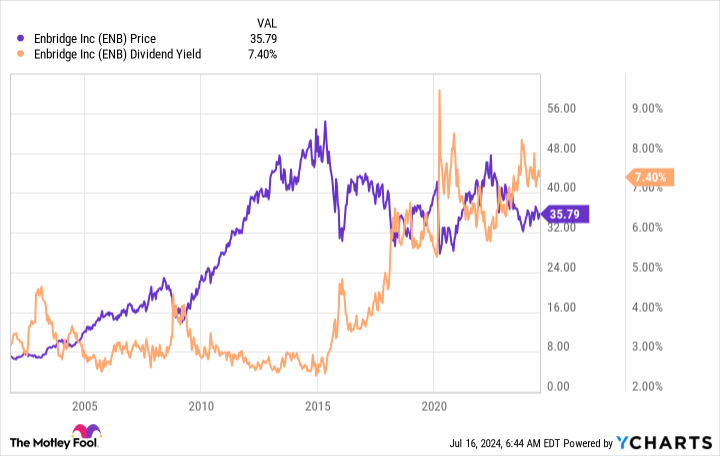

Enbridge (NYSE: ENB) isn’t an exciting company, but that’s actually one of the biggest draws here. That and an ultra-high dividend yield of around 7.4%. But to really understand why you’ll be glad you bought this stock in a few years, you need to dive deeper into its business and see how it returns value to investors over time.

Enbridge is more than a midstream giant

The energy sector is known for being volatile, but not every company in the sector deserves that label. Upstream (drilling) and downstream (refining and chemicals) companies are often quite volatile, but midstream companies like Enbridge tend not to be. That’s because midstream companies own the energy infrastructure (such as pipelines) that connects the upstream to the downstream and the rest of the world, and they largely charge fees for the use of their assets.

Enbridge is essentially a toll taker. And since oil and natural gas are essential to the smooth functioning of the world, demand remains strong even then energy the prices are weak. Oil pipelines account for about 50% of earnings before interest, taxes, depreciation, and amortization (EBITDA), while natural gas pipelines account for about 25%. That’s where the next interesting fact about Enbridge emerges.

The rest of the energy giant’s business comes from regulated natural gas companies (22% of EBITDA) and investments in renewable energy (3%). Natural gas burns cleaner than coal or oil and is seen as a transition fuel. Enbridge recently agreed to purchase three natural gas companies Dominion energy, increasing exposure to this energy niche from 12% to over 22%. Regulated utilities are given a monopoly in the regions they serve in exchange for requiring government approval of rates and investment plans. This leads to slow and steady growth over time. In short: Enbridge’s business operations are even more reliable thanks to this investment.

Then there’s the renewable energy sector, which is quite small compared to the rest of the business. But clean energy is also still a relatively small part of the global energy pie. Enbridge’s expansion into space is essentially an attempt to use carbon fuel profits to change with the world as clean energy becomes increasingly important over time. It provides a kind of protection for investors who are not yet ready to jump into renewable energy, but recognize its increasing role in the world.

What can investors expect from Enbridge?

So Enbridge is a boring midstream company that is slowly turning its operations in a cleaner direction. That’s not exactly an exciting story until you take into account the enormous dividend yield of 7.4%. Most investors expect the stock market as a whole to deliver returns of roughly 10% per year, so Enbridge’s dividend alone puts you at roughly three-quarters.

In the meantime, that dividend is supported by a balance sheet with an investment-grade rating. And the distributable cash flow payout ratio is right in the middle of management’s target range of 60% to 70%. The dividend has also been increased annually for 29 years in a row. This is a reliable dividend stock and there is no reason to believe the dividend is in jeopardy. In fact, it seems very likely that slow and steady dividend growth in the low single digits is a reasonable expectation.

So if the dividend grows roughly in line with inflation, at around 3%, the total return investors can expect is likely to be around 10%, adding the current yield of over 7% to the dividend increase of around 3%. Normally, stocks rise over time along with their dividends to keep returns constant, so market-like returns from these high-yield stocks are not an unrealistic expectation. That’s hard to complain about, especially if you reinvest your dividends, which allows them to grow over time.

The base case for Enbridge is good

It seems likely that Enbridge can manage to just plod along with what it’s doing. That will be enough to provide investors with solid returns, as mentioned above. But what’s interesting here is that Enbridge’s dividend yield is historically high today. So it appears that the stock is trading at a low price.

It is entirely possible that this situation will not change and that revenue has simply increased to a new range to reflect Enbridge’s business as it stands today. However, if Wall Street suddenly becomes more interested in the company, investors who buy today will get a boost from increased demand for the stock. The base case is that Enbridge’s dull businesses deliver roughly market-like returns, while the upside could be much higher. That seems like an attractive risk/reward balance that you’ll regret missing if you don’t jump on board soon.

Should you invest $1,000 in Enbridge now?

Consider the following before purchasing shares in Enbridge:

The Motley Fool stock advisor The analyst team has just identified what they think is the 10 best stocks for investors to buy now… and Enbridge wasn’t one of them. The ten stocks that survived the cut could deliver monster returns in the coming years.

Think about when Nvidia created this list on April 15, 2005… if you had $1,000 invested at the time of our recommendation, you would have $722,626!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including portfolio building guidance, regular analyst updates and two new stock picks per month. The Stock Advisor is on duty more than quadrupled the return of the S&P 500 since 2002*.

*Stock Advisor returns July 15, 2024

Ruben Gregg Brouwer has positions in Dominion Energy and Enbridge. The Motley Fool holds and recommends positions in Enbridge. The Motley Fool recommends Dominion Energy. The Motley Fool has one disclosure policy.

In a few years, you’ll wish you had bought these undervalued high-yield stocks was originally published by The Motley Fool