Table of Contents

Everyone knows Warren Buffett’s monster Apple (NASDAQ: AAPL) investment. The huge $100 billion winner – which Buffett recently shortened – has been cited time and time again as one of the Berkshire Hathaway‘s best investments. However, the investment has been held for less than ten years, while Buffett has been investing for more than sixty years.

Buffett bought and held American Express (NYSE:AXP) many years longer than Apple. And yet few people talk about this huge winning investment. Although the stock is up more than tenfold since Buffett’s initial purchase, the shares still look cheap today. This is why American Express is poised to crush the market again and could be Buffett’s top player until 2030.

American Express: one of Buffett’s favorite brands

American Express operates one of the few credit card networks in the world. Unlike other networks such as Visa And MasterCardAmerican Express acts as a bank and actually issues its own credit cards. This vertically integrates digital payments, making American Express a unique company in the credit card world.

Catering to a wealthier customer base, the company has built a premium brand that has been refined for decades. It offers high-fee credit cards, such as the American Express Platinum Card, which has an annual fee of $695 per year. People are willing to pay these costs for the great travel benefits, cashback deals and other perks of the American Express ecosystem. As a classic network effect, it would be virtually impossible to remove American Express from the payments ecosystem and replace it, making it a wide-moat company.

Buffett likes top brands like American Express, Apple and Coca-cola. It’s no surprise that Berkshire Hathaway still owns over 20% of the company. The company made its first investment in 1991. Since then, American Express has achieved a total return of almost 8,000%, which is better than Coca-Cola during the same period.

Growing card members, growing international acceptance

About ten years ago, American Express was going through a rough patch. It struggled to acquire new users and lost a huge contract for the Costco Wholesale credit card partnership.

Since then, with new management at the helm, the company has gotten back on track. The total number of cardholders is growing again and has been the case for a number of years. Last quarter, the company added 3.3 million new cards, an acceleration from an increase of 3 million in the same quarter a year ago. New cards are the lifeblood of American Express’s business, so it’s great to see new customers joining the platform. In the coming decades, these customers should add a lot of value to American Express’s business as these wealthy customers make purchases with these cards and pay the high annual fees.

To keep up with this growth, American Express is aggressively investing in growing the number of places that accept American Express card payments. This is the other lifeblood of the payments industry. If a merchant doesn’t accept your credit card as payment, you won’t make any money because shoppers can’t use their card to make the purchase. Since 2017, the company has quadrupled the number of international acceptance locations, which will drive even more payments growth in the coming years. It today has virtual acceptance parity with Visa and Mastercard in the United States.

Buy this ultimate dividend grower and never sell

Through higher card fees, payment volume, international acceptance and more credit card lending, American Express believes it can grow its revenues 10% annually over the long term. Management believes earnings per share (EPS) can grow even faster.

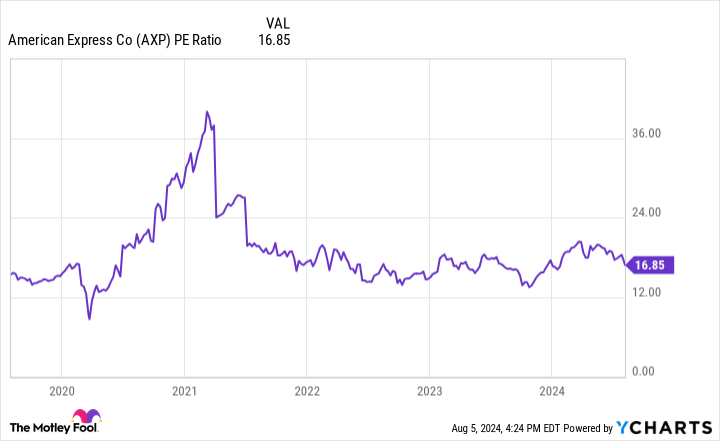

This growth will – if you agree with management – give American Express a lot of capacity to grow its dividend payments. The stock currently has a dividend yield of 1.23%, which seems quite low. But the stock isn’t hugely expensive and trades at a price-to-earnings (P/E) ratio of 17, which is below market value. Over the past decade, American Express’s dividend per share has grown 165%.

If revenue and earnings continue to grow at 10% or more, I think the stock can more than double its dividend per share again in 2030. Combined with a low starting valuation, I think American Express could be Buffett’s best performing stock year to date. 2030.

Should You Invest $1,000 in American Express Now?

Consider the following before buying shares in American Express:

The Motley Fool stock advisor The analyst team has just identified what they think is the 10 best stocks for investors to buy now… and American Express wasn’t one of them. The ten stocks that made the cut could deliver monster returns in the coming years.

Think about when Nvidia made this list on April 15, 2005… if you had $1,000 invested at the time of our recommendation, you would have $643,212!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including portfolio building guidance, regular analyst updates, and two new stock picks per month. The Stock Advisor is on duty more than quadrupled the return of the S&P 500 since 2002*.

*Stock Advisor returns August 6, 2024

American Express is an advertising partner of The Ascent, a Motley Fool company. Brett Schafer has no position in any of the stocks mentioned. The Motley Fool holds positions in and recommends Apple, Berkshire Hathaway, Mastercard and Visa. The Motley Fool recommends the following options: long January 2025 $370 calls on Mastercard and short January 2025 $380 calls on Mastercard. The Motley Fool has one disclosure policy.

Prediction: This stock will be Warren Buffett’s best performing stock in 2030 was originally published by The Motley Fool